Live Spot Gold

Bid/Ask

2,639.202,640.20

Low/High

2,613.202,653.20

Change

-0.20-0.01%

30daychg

+7.10+0.27%

1yearchg

+594.30+29.06%

Silver Price & PGMs

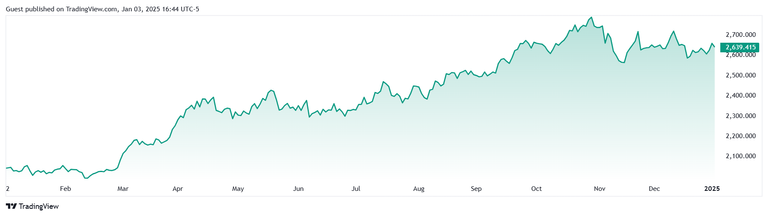

Spot gold kicked off the year hovering around $2,000 per ounce, and the yellow metal dipped as low as $1,992 in mid-February before getting a Valentine’s Day boost back above the 2K level. But it was the end of February that started its steep ascent, as spot gold gained over $60 during the last 2 days of the month and broke above $2,100 on the first trading day of March.

Once again, a period of consolidation at elevated levels was followed by a late-month rally that saw gold prices break above $2,200 during the final days of trading, and by mid-April, the yellow metal was drawing close to $2,400 per ounce. But gold traders were not yet ready for these heights, and spot gold slid back below $2,300 at the end of April.

May brought renewed optimism to metals markets, and on the 16th, spot gold broke decisively through the $2,400 per ounce resistance level. But after topping out near $2,426, gold once again entered another period of consolidation, this one proving to be the longest-lasting of 2024.

But on June 10th, gold once again breached the $2,400 per ounce level, and this time, it found support, whereupon it began its most steady climb of the year, which saw the yellow metal ladder higher through the late summer and early fall to top out at a new all-time high of $2,788.54 per ounce on October 30.

After a shallow pullback, it was the election of Donald Trump on November 5th that ultimately knocked gold off its pedestal, as the yellow metal fell from $2,743 per ounce on November 4th all the way down to the low $2,560s just 10 days later.

But gold prices found fresh support as the President-elect’s threats of tariffs and trade wars combined with renewed inflation fears once again drove spot prices back above $2,700 per ounce, and even though the precious metal was unable to challenge its October highs, apart from a few dips, support at $2,600 per ounce held through the balance of 2024.

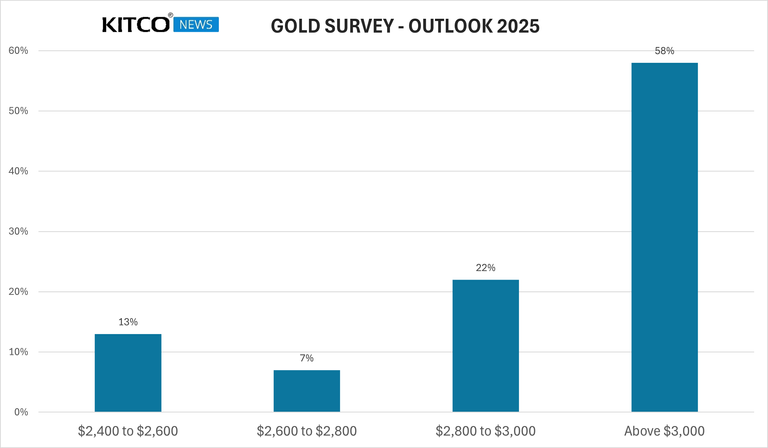

The Kitco News Annual Gold Survey showed strong belief in the yellow metal’s bullish potential on the part of retail traders, while the big banks and industry experts mostly expect continued strength from gold prices in 2025.

457 retail investors participated in the Kitco News Annual Gold Survey, with a strong majority of Main Street predicting the yellow metal will set a new all-time high as it trades above three thousand dollars per ounce in 2025.

266 retail traders, fully 58%, expect gold to trade above $3,000 per ounce level next year, with the current all-time high of $2,788.54 set on October 30, 2024. Another 22%, or 103 Main Street investors, predicted gold prices will trade between $2,800 and $3,000 in 2025, while only 7%, or 30 participants, expect gold to top out somewhere between $2,600 and $2,800. The remaining 58 retail traders, representing 13% of the total, think gold prices will drop back into the $2,400 to $2,600 per ounce range seen in late summer and early fall of 2024.

Compared to Main Street, Wall Street analysts, while bullish on gold, have a slightly more cautious view.

Chantelle Schieven, Head of Research at Capitalight Research, told Kitco News in a recent interview that gold is continuing to hold its own and the recent consolidation is the first major correction the precious metal has seen in a year.

“I am not at all concerned with the volatility we are seeing,” she said. “I think this breather is healthy for the market.”

At the start of 2024, Schieven was the most bullish analyst among those surveyed by the London Bullion Market Association in its annual forecast. She predicted that gold would hit $2,400 an ounce this year, a level it surpassed by nearly $400. Looking ahead, Schieven said she thinks gold still has a lot more room to run.

“I am still as bullish on gold for 2025 as I was for 2024,” she said, but added that her bullishness is tempered with patience as she expects the current consolidation phase to last a few months. She said she sees gold trading between $2,500 and $2,700 in the first half of the year, but expects gold prices to surpass $3,000 an ounce in the second half of 2025.

Schieven said she expects to see slower economic growth in H2 2025 due to a global trade war and geopolitical uncertainty. She also sees inflation holding above 3%.

“A mild recession with higher inflation should be the perfect environment for gold,” she said, adding that there is a strong investment case for gold to represent about 10% of an investor’s portfolio.

Fawad Razaqzada, Market Analyst at City Index, wrote in their 2025 Gold Fundamental Outlook Preview that while U.S. dollar strength, higher bond yields, equity outperformance, and weaker Asian demand will work against gold this year, a number of factors still support the yellow metal’s journey to $3,000 per ounce in 2025.

Razaqzada wrote that a key driver of the 2024 gold rally was the expectation that central banks would lower interest rates as inflation fell, but these expectations have since been reined in.

“[M]onetary policy is likely to remain tight in early 2025, potentially supporting bond yields and the US dollar— two factors that often work against gold’s appeal,” he said.

Higher bond yields also have a significant impact on investment demand for the yellow metal, as they raise the opportunity cost of holding non-yielding assets like gold. “Concurrently, the US dollar’s resilience, bolstered by hawkish central bank policies and surprisingly strong economic data, has made gold relatively more expensive for buyers using weaker currencies,” he said. “These dynamics could limit gold’s upside potential in the year’s first half.”

China and India, the world’s two largest consumer markets for gold, are also facing domestic challenges that could dampen demand for the precious metal, he added.

Even setting aside the currency issues, Razaqzada said there are major geopolitical risks to consider. “Potential US tariffs on Chinese goods could exacerbate economic pressures, while increased haven demand stemming from global uncertainties may only partially offset these headwinds,” he said.

The recent positive correlation between gold and risk assets also complicates the picture.

“Investor sentiment in 2024 leaned heavily toward riskier assets, initially fuelled by rate-cut hopes and then optimism following Trump’s re-election,” Razaqzada said. “Bitcoin, XRP, and other cryptocurrencies enjoyed meteoric rises, while equity indices like the S&P 500 and German DAX reached all-time highs. This shift in risk appetite reduced the allure of safe-haven assets like gold towards the end of the year, which typically thrive during periods of economic uncertainty – although, in more recent years, both gold and the S&P 500 have been going in the same general direction.”

“Therein lies the problem with gold: can it decouple from risk assets?”

But whether equity markets rise or fall, Razaqzada believes that gold’s long-term appeal will remain intact. “Inflation continues to erode the purchasing power of fiat currencies, reinforcing gold’s status as a store of value,” he noted. “Moreover, geopolitical tensions—from the Middle East to potential trade wars—could rekindle haven demand, providing a counterbalance to last year’s risk-on sentiment.”

The question on the minds of many investors is whether the gold price can break the 3k level in this environment. Razaqzada believes that it can.

“Despite short-term challenges, a $3,000 gold price target remains feasible,” he said, adding that any corrections or consolidations in the early part of 2025 will likely set the stage for another rally in the second half.

Nicky Shiels, Head of Research & Metals Strategy at MKS PAMP, said in her 2025 precious metals outlook that she expects gold to trade within a fairly wide range between $2,500 and $3,200 an ounce, with the precious metal’s fate largely determined by the Federal Reserve.

“Gold prices at $3,000+ or $2,500- depend on whether the Fed is ahead or behind the Trumpflation curve; we expect them to be behind, leading to falling real rates and a softer US$ in the latter half of the year,” she said. “Structurally, the positive feedback loop of high-for-longer inflation, ongoing deglobalization, currency debasement, central bank dedollarization, messy and unpredictable geopolitics, unsustainable global debt paths, and an under-owned general investor community ensures that gold remains a safe asset diversifier.”

Although gold will enjoy solid fundamental support in 2025, Shiels noted that the probability of a bear market is higher than that of a bullish scenario. She sees a 30% chance of gold trading closer to $2,500 an ounce next year as President-elect Donald Trump drives American exceptionalism with pro-growth policies such as tax cuts and deregulation.

At the same time, America-first policies are expected to push consumer prices higher, forcing the Federal Reserve to slow its easing cycle, even as it lags behind the inflation curve. Shiels also cautioned gold investors that the new administration’s focus on cryptocurrencies could divert some investors away from the precious metals market next year.

Meanwhile, MKS assigns only a 20% chance of gold prices exceeding $3,000 an ounce in 2025.

ING commodities strategist Ewa Manthey wrote in her 2025 gold forecast that a bullish macro picture combined with continued geopolitical risk and strong sovereign buying will drive gold prices to new highs in 2025.

“The main question for the gold market now is the pace at which the Fed will ease its policy following Donald Trump’s win in the US presidential election; the inflationary impact of Trump’s policies could lead to fewer rate cuts than previously expected,” Manthey said. “Our US economist, James Knightley, thinks that the US central bank will cut by 25bp again in December – but the outlook thereafter is less clear, and there is a strong chance of a pause at the January FOMC meeting.”

Knightly has lowered his 2025 rate cut forecast from 50bp to 25bp per quarter beginning in Q1 2025, with rates bottoming at 3.75% in Q3 2025.

ING expects central bank gold demand to remain strong during the coming year, which will continue to support historically high gold prices.

“Central banks have continued to boost their gold reserves, although the pace of buying slowed in the third quarter, with high prices deterring some buying,” Manthey wrote. “Central banks’ healthy appetite for gold is also driven by concerns from countries about Russian-style sanctions on their foreign assets in wake of decisions made by the US and Europe to freeze Russian assets, as well as shifting strategies on currency reserves.”

ING’s overall position is that the gold rally has further to run in 2025, and the bank expects prices to average close to this year’s all-time high in Q1-Q2 2025.

“We believe gold’s positive momentum will continue in the short to medium term,” Manthey said. “The macro backdrop will likely remain favourable for the precious metal as interest rates decline and foreign-reserve diversification continues amid geopolitical tensions, creating a perfect storm for gold.”

“In the longer term, Trump’s proposed policies – including tariffs and stricter immigration controls, which are inflationary in nature – will limit interest rate cuts from the Federal Reserve,” she concluded. “A stronger USD and tighter monetary policy could eventually provide some headwinds to gold. However, increased trade friction could add to gold’s haven appeal.”

ING projects the spot gold price will average $2,800 per ounce in Q1 and Q2, before pulling back to $2,750 in Q3 and $2,700 in Q4, for an average price of $2,760 per ounce for 2025.

Commodity analysts at BMO Capital Markets predicted in their 2025 outlook that gold will remain a key asset in investor portfolios in 2025, and noted that the potential for a global trade war will continue to fuel geopolitical uncertainty, providing further momentum for the gold market.

“We expect the push for de-dollarization of trade to re-emerge in Q2 as trade friction grows, and this could push gold to new nominal highs,” the analysts said.

BMO sees gold prices averaging around $2,750 an ounce in 2025, up 3% from its previous estimate. In a quarterly breakdown, the analysts expect prices will peak during the summer, averaging $2,850 an ounce in the third quarter.

The analysts also expect China to continue to be a dominant player in the gold market.

“We do not see global financial systems as being fully prepared for this, and hence gold is once more being pulled back into the monetary system,” the analysts said.

BlackRock, the world’s largest asset manager, said in their 2025 Global Outlook that the geopolitical landscape will be characterized by intensifying fragmentation in the year ahead, which is likely to accelerate de-dollarization and support gold purchases.

“Elevated global tensions are accelerating the rewiring of supply chains,” wrote Tom Donilon, Chairman of the BlackRock Investment Institute, “and the formation of competing geopolitical and economic blocs. A second Trump administration is likely to reinforce those trends. We see that playing out in tech, energy and financial markets.”

Donilon wrote that the “rewiring of globalization” is also being seen in reserve currencies. “As the world divides into competing blocs, and the U.S. and Western governments lean on sanctions and other restrictions for their policy response, some countries are shifting their reserves out of U.S. dollars into gold and other assets while increasingly conducting trade finance in non-dollar currencies,” he said.

Samara Cohen, BlackRock’s Chief Investment Officer of ETFs and Index Investments, said that investors will need to rely on diversifiers like gold and Bitcoin to manage risk in this increasingly fragmented world.

“The erratic correlation between stock and bond returns has defined the new regime – and government bonds have become a less reliable cushion against equity selloffs as a result,” she wrote. “We see the potential for other diversifiers, old like gold and new like bitcoin, to step in. This is not about replacing long-term bonds to find diversification but instead seeking new and distinct sources of risk and return.”

“Gold has surged as investors seek to bolster portfolios against higher inflation, and some central banks seek alternatives to major reserve currencies,” Cohen concluded. “We think it is key to monitor how the performance of these alternatives changes relative to traditional asset classes – and be nimble in using them.”

Commodities strategists at TD Securities noted in their 2025 Outlook that gold prices may see a near-term correction as investors reduce their long positions, but persistent inflation and geopolitical instability will ensure that the yellow metal will not see a rout in 2025.

TD believes that the main drivers of gold‘s record-breaking 2024 rally were “expectations of a rapid decline in the fed funds target rate, US political uncertainty, geopolitical risks, and strong buying activity by central banks and investors.”

“The impact of these supportive factors on gold has now likely peaked, with rate cut projections having been sharply reduced in the aftermath of the US elections as the GOP painted the American political map red, raising inflation risks on the horizon at a time when economic growth remains firm,” the analysts warned. “Given the change in the interest rate trajectory, a firm USD, and a slower uptake of physical metal by central banks, coin and bar investors, the market may very well be ready to consolidate the recent gains.”

Under these circumstances, TD Securities said they would not be surprised to see some profit-taking from traders with significant long gold positions as they look ahead at higher bond yields, strong equity markets, and a changing geopolitical environment. “Significant macro fund liquidations may have already hit the tapes, limiting the scope for subsequent selling activity, but the macro outlook no longer favors extreme long positioning given lower odds of an ‘overly easy’ policy on the horizon,” they wrote.

The analysts said that while there are risks of a continued correction, there’s also plenty of uncertainty to support gold’s status as a hedge, including questions surrounding the Fed independence under the new GOP regime in Washington.

“For the first time in decades, the US President-elect brings diverging ideas about whether the Fed should remain independent in setting monetary policy,” they wrote. “While we see low odds that President Trump would be able to remove Chair Powell from office, he may be able to appoint a more dovish Fed Chair after Powell’s term ends in May 2026. The notion of a “shadow Fed Chair” further risks threatening the Fed’s independence.”

TD Securities’s detailed forecasts have spot gold trading at $2,675 per ounce in the first quarter of 2025 and topping out at $2,700 in Q2, before dropping to $2,625 in both Q3 and Q4. Their outlook for the following year predicts more price moderation, as they see the yellow metal starting 2026 trading at $2,600 throughout the first half and $2,525 in the second half.

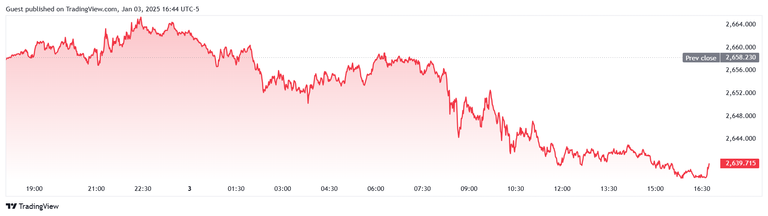

After trading as high as $2,665.40 during the Asian session, gold prices have slid steadily lower on Friday, though they have held comfortably above the $2,600 per ounce level throughout the day.

Spot gold last traded at $2,639.71 per ounce for a loss of 0.70% on the day.

Posted by:

Jack Dempsey, President

401 Gold Consultants LLC

jdemp2003@gmail.com