Late report Wednesday , July 17th, 2024

SPOT MARKET IS OPEN (WILL CLOSE IN 20 HRS. 37 MINS. )

Live Spot Gold

Bid/Ask

2,457.802,458.80

Low/High

2,456.102,461.70

Change

0.00–

30daychg

+136.30+5.87%

1yearchg

+481.60+24.37%

Silver Price & PGMs

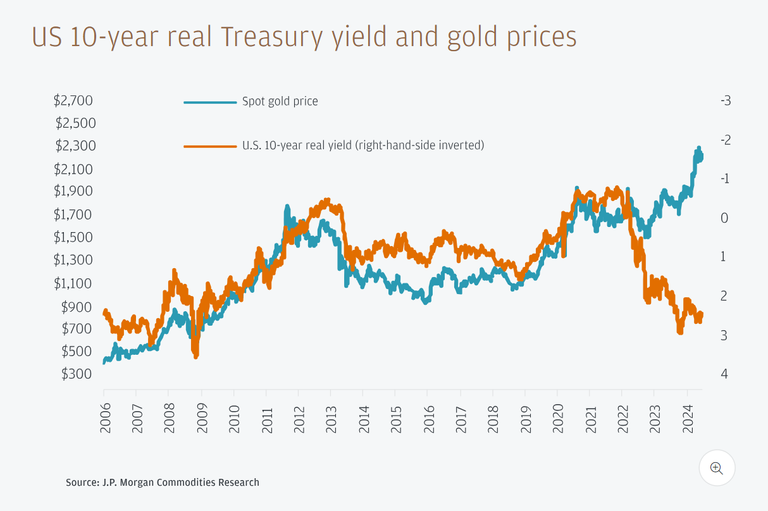

(Kitco News, Wed. July 17th, 2024) – Gold has decoupled from the interest rate outlook and real yields, and even though prices have already risen sharply, the structural bull case for gold remains intact, according to commodity strategists at J.P. Morgan.

The strategists noted in a report published on July 15 that a weaker U.S. dollar and lower U.S. interest rates traditionally boost the appeal of non-yielding bullion, but since early 2022 gold’s relationship with real yields has been breaking down.

“Gold’s resurgence has come earlier than expected, as it further decouples from real yields,” said Gregory Shearer, Head of Base and Precious Metals Strategy at J.P. Morgan. “We have been structurally bullish gold since the fourth quarter of 2022 and with gold prices surging past $2,400 in April, the rally has come earlier and has been much sharper than expected. It has been especially surprising given that it has coincided with Fed rate cuts being priced out and U.S. real yields moving higher due to stronger labor and inflation data in the U.S.”

“Amid fraying geopolitics, increased sanctioning and de-dollarization, we observe an increased appetite to buy real assets including gold,” Shearer said. Recent data also shows reluctance among physical holders to sell their gold despite the strong price gains, underscoring the structurally bullish drivers irrespective of U.S. real yields.

With gold prices already hovering near all-time highs, J.P. Morgan sees further potential for the yellow metal as U.S. rates begin to fall.

“Many of the structural bullish drivers of a real asset like gold — including U.S. fiscal deficit concerns, central bank reserve diversification into gold, inflationary hedging and a fraying geopolitical landscape —have lifted prices to new all-time highs this year despite a stronger U.S. dollar and higher U.S. yields, [and] will likely remain in place regardless of the U.S. election outcome this autumn,” said Natasha Kaneva, Head of Global Commodities Strategy at J.P. Morgan. “Nonetheless, precious metals markets will be focused on any potential policy changes that could accentuate or alter one or more of these themes.”

Shearer reiterated the firm’s strong positive position on the medium-term outlook for gold as well as silver prices. “Across all metals, we have the highest conviction on a bullish medium-term forecast for both gold and silver over the course of 2024 and into the first half of 2025, though timing an entry will continue to be critical,” he said.

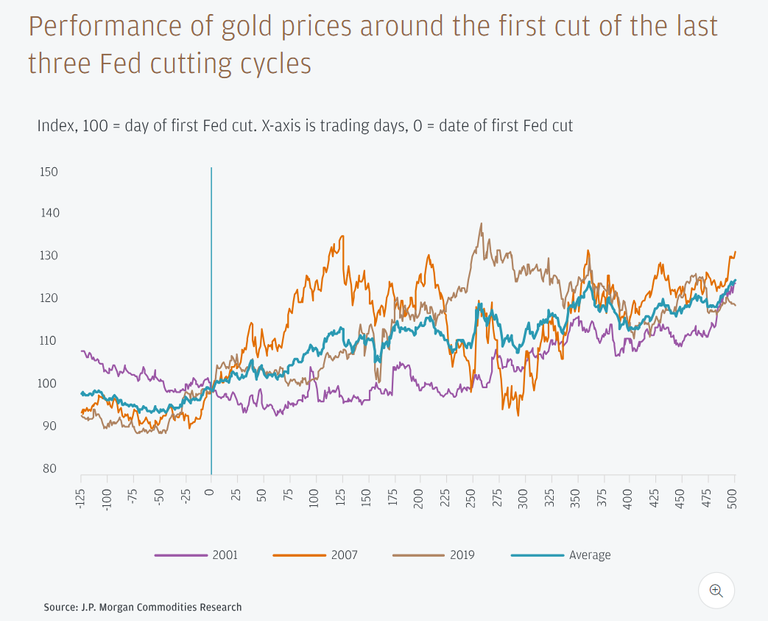

The report said that any retracement in the coming months will provide investors with “an opportunity to begin positioning for further strengthening” ahead of the Fed’s expected rate cuts.

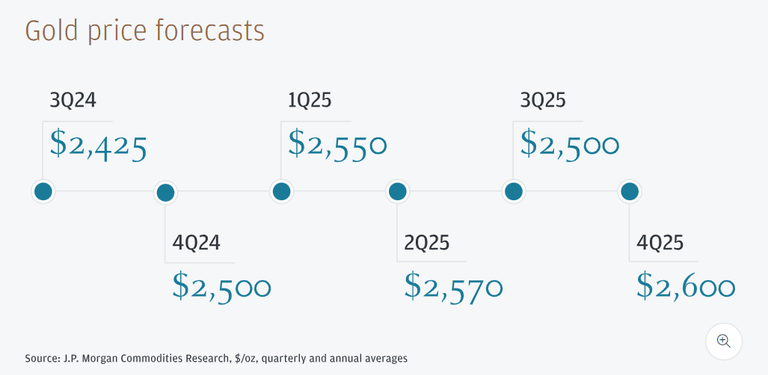

The firm has also upgraded its gold price targets for both 2024 and 2025. According to the latest J.P. Morgan Research estimates, gold prices are now expected to reach $2,500 per ounce by the end of 2024. The new estimates assume the Fed rate-cutting cycle will begin only in November, while markets are fully priced in for a September cut.

“The direction of travel is still higher over the coming quarters, forecasting an average price of $2,500/oz in the fourth quarter of 2024 and $2,600/oz in 2025, with risk still skewed toward an earlier overshoot,” Shearer said.

The new price predictions are based on J.P. Morgan’s updated economic forecasts, which see U.S. core inflation moderating to 3.5% in 2024 and 2.6% in 2025.

Outside of near-term mean reversion, the biggest bearish risk the firm sees for the yellow metal is if the Fed becomes much more aggressive in its targeting of inflation.

“While we still think it’s a tail risk, a transition to much more hawkish Fedspeak that prompts the market to begin pricing a switch back to further hikes could drag on gold, even with the recent decoupling from yields,” Shearer said. “This could eventually set up an even larger rally if it pushes the economy toward a hard landing, but the road there would likely be a lot bumpier than our forecasts envision.”

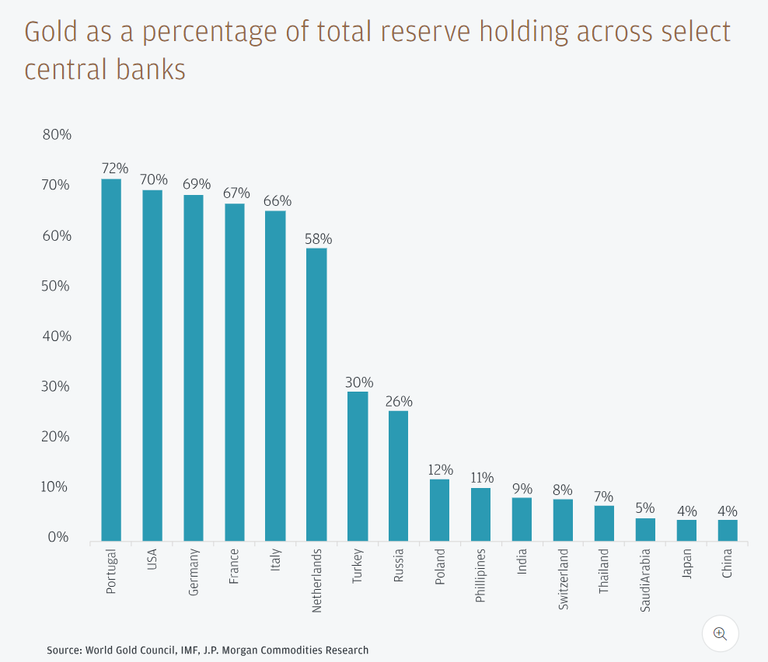

The firm also expects strong central bank demand to continue through 2024, noting that the latest data from the World Gold Council showed 290 tonnes of net purchases in Q1, the fourth strongest quarter of purchases since the current run of sovereign buying binge began in 2022.

“This also came in around 36% higher than the quarterly pace (around 213 tonnes) implied by J.P. Morgan Research’s annual estimates of 850 tonnes in 2024,” the report said. “The 70-tonne increase in net purchases versus the fourth quarter of 2023 is also despite a 5% quarter-on-quarter increase in the average price of gold.”

“Overall, the vigorous level of central bank purchasing, as well as the continued ascent in gold prices since the end of the first quarter, has us thinking about the price sensitivity of central bank demand,” Shearer said. “We think the price level of gold has minimal impact on long-term central bank acquisition plans, however, price changes do appear to influence the pace and cadence of net purchasing.”

J.P. Morgan also sees increased investor appetite in the physical gold market as a major flow contributor to future gold rallies.

“Total ETF holdings in gold have fallen steadily since mid-2022, but so have London vault holdings of gold as demand from EM central banks and physical consumers have physically offset ETF outflows,” the report noted. “A re-lengthening of investor ETF holdings triggered by the onset of a cutting cycle could quickly act to tighten up the physical gold market and is expected to be positive for bullion and supportive of a climb in prices in the second half of 2024.”

“While gold price movements may be fully decoupled from real yields and Fed pricing for now, we still think this would add an extra pillar of support later this year mainly through an eventual shift back toward retail ETF inflows, as money market funds become less attractive,” Shearer concluded. “Gold prices have already jumped higher even as ETF holdings have continued to sag, and a turnaround here could be quite bullish, driving another sustained leg higher in prices.”

Jack Dempsey, President

401 Gold Consultants LLC

jdemp2003@gmail.com