Live Spot Gold

Bid/Ask

3,185.703,187.70

Low/High

3,173.103,257.80

Change

-63.50-1.95%

30daychg

-24.30-0.76%

1yearchg

+832.50+35.40%

Silver Price & PGMs

(Kitco News, Wed. May 14th, 2025) – China’s gold market posted one of its strongest performances of all time in April, with prices, physical and investment demand all sky-high, but demand may wane as U.S.-China tensions ease, according to Ray Jia, Research Head, China at the World Gold Council (WGC).

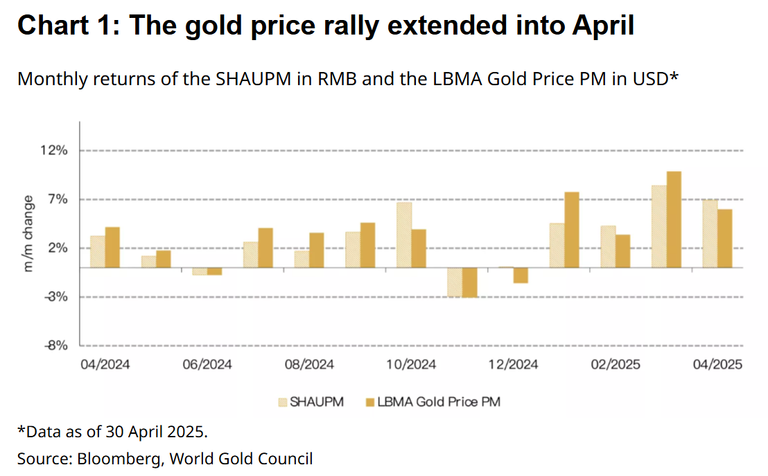

Jia noted that global gold prices continued their rise in April, and this strength was reflected in the Chinese market. “Our model shows that a weaker dollar, elevated geopolitical/economic uncertainties and strong gold ETF inflows drove gold up,” he said. “While the LBMA Gold Price PM in USD saw its strongest April since 2011, the SHAUPM in RMB recorded its highest April return in 19 years.”

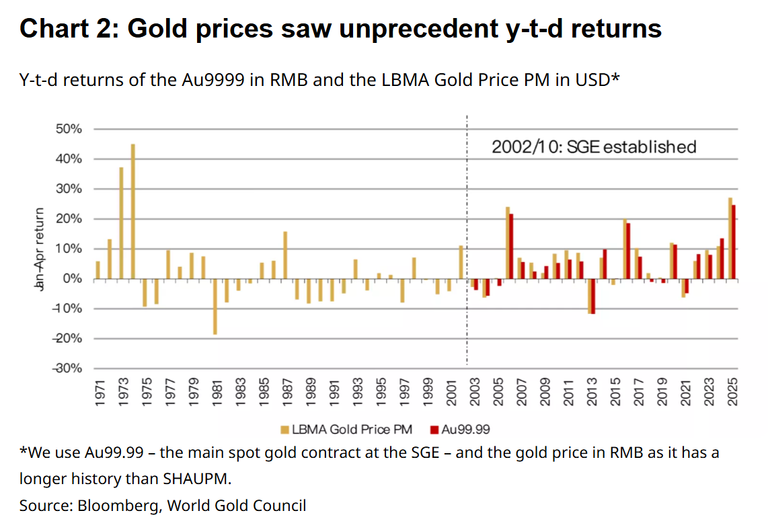

Jia said that the RMB gold price has seen a cumulative return of 24%, marking the strongest January to April performance on record. “And the LBMA Gold Price PM soared 27% during the same period,” he added, “The difference is mainly a result of a stronger RMB, which has appreciated 1% so far in 2025.”

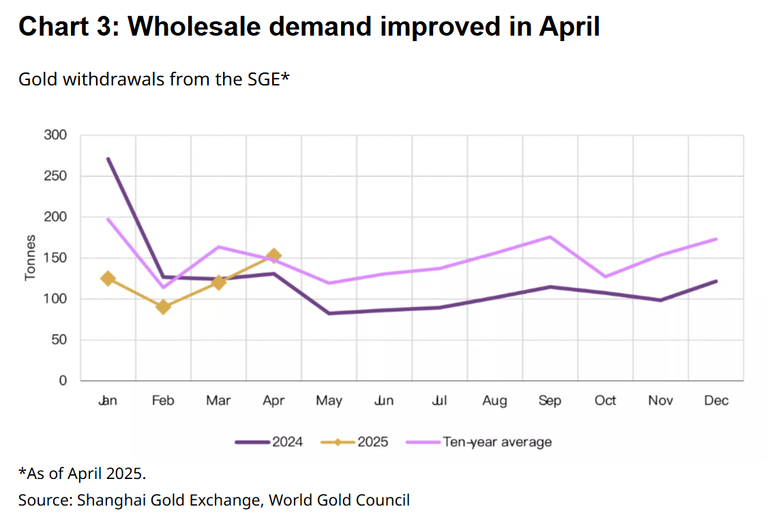

Wholesale demand also continued to recover last month. “The industry withdrew 153t gold from the SGE, a rise of 27% m/m and 17% y/y,” Jia said. “The improving wholesale gold demand is also reflected in the rising local gold price premium, which averaged US$37/oz in April, significantly higher than March’s US$2/oz.”

He said the strength in April wholesale demand was supported by two key factors.

“Continued robustness in bar and coin sales amid strong investor buying,” with gold remaining “a top-performing asset in China as US-China trade tensions intensified,” as well as jewellers re-stocking for the early May Labour Day Holiday following lower-than-usual Q1 withdrawals.

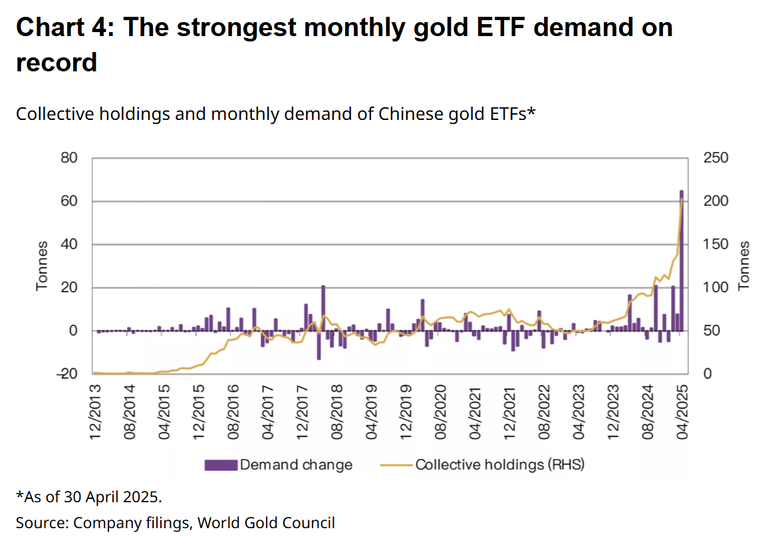

But ETF demand was the real standout in April, with Chinese gold ETFs posting their strongest month on record, adding RMB49 billion, or $6.8 billion.

“The third consecutive monthly inflow and the continued surge in the gold price lifted their total AUM to RMB158bn (US$22bn); a rise of 57% in April and the highest month-end value ever,” Jia said. “Meanwhile, holdings surged by 65t to 203t, also a record high.”

“This unprecedented demand surge was mainly driven by the attractive local gold price performance, US-China trade war concerns and falling local bond yields amid intensified easing expectations,” he added. “During the first four months of 2025 Chinese gold ETFs’ total AUM and holdings have jumped by 125% and 77%, respectively.”

Jia warned that Chinese ETF demand remains strong in May but has slowed considerably compared to April. “This is likely due to investors having mostly priced in previous trade uncertainties – which have eased following the US-China Geneva trade talk – and a stabilisation of the local gold price,” he said.

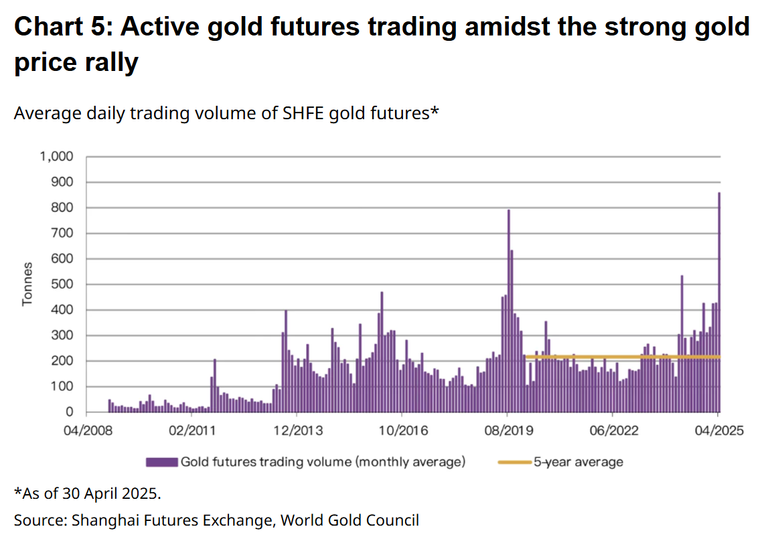

Chinese investor interest in gold futures also reached unprecedented levels in April. “The average daily trading volume of SHFE’s gold futures doubled m/m to reach a record 859t,” he said. “We believe amplified gold price volatility and the strong gold price performance attracted trader attention, pushing volumes of gold futures notably higher.”

And while gold futures trading cooled somewhat in early May, the average volume during the first five trading days remained near the record high at 756 tonnes per day. “This marks traders’ continued enthusiasm in gold futures despite the price adjustment recently,” he added.

China’s central bank also contributed to the demand in April, with the PBoC’s gold purchasing streak now extending to six months.

“Reported gold reserves in China rose 2.2t in April, lifting the total to 2,295t, or 6.8% of overall reserve assets,” Jia noted. “In value terms, China’s gold reserves rose to US$243.6bn, 6% higher m/m. So far in 2025, China has announced an increase of 14.9t in its official gold holdings.”

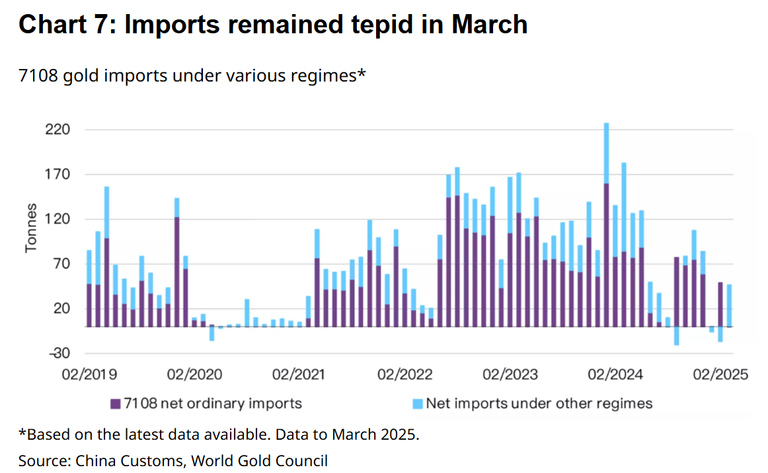

Imports, on the other hand, continued their weak start to 2025 with the latest data showing China importing 46 net tonnes of gold in March. “Despite a 14t m/m rebound, this was well below last March’s 183t,” he said. “And Q1 total imports amounted to 73t, the lowest since 2021 when COVID-related restrictions limited imports, and far below the 545t level in Q1 2024.”

Jia said that a key reason for the slowdown was weaker demand for gold jewellery during the quarter, which “helped squeeze the local gold price premium, at times pushing it to a discount, which further discouraged gold importers.”

Looking ahead, Jia said WGC analysts “expect gold jewellery consumption, in tonnage terms, to remain tepid as it enters its off season after the five-day Labour Day Holiday, although the recent price adjustment could provide some support.”

“Gold investment demand may also cool in the near term, possibly due to profit taking, the range-bound price movements and cooling US-China trade tensions,” he concluded. “But in the longer term, gold’s investment demand should be well supported amid its attractive performance, lingering global economic and geopolitical risks, as well as institutional allocations from Chinese insurers.”

Posted by:

Jack Dempsey, President

401 Gold Consultants LLC

jdemp2003@gmail.com