Live Spot Gold

Bid/Ask

2,904.302,905.30

Low/High

2,880.302,945.00

Change

-3.00-0.10%

30daychg

+214.00+7.95%

1yearchg

+888.20+44.06%

Silver Price & PGMs

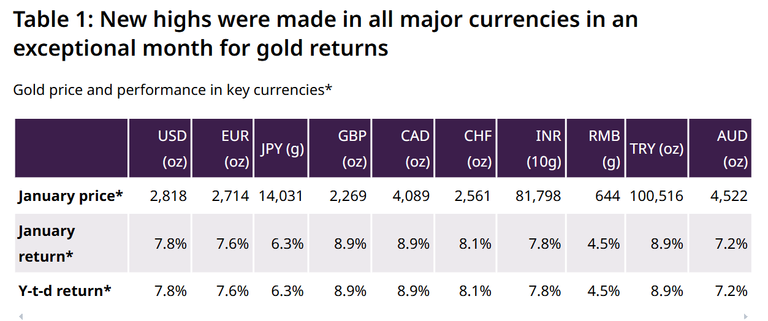

(Kitco News, Tuesday. Feb. 11th, 2025) – Gold prices finished last month at an all-time high in every major currency, and developments in Germany and China could provide further momentum this month, according to the World Gold Council (WGC).

In their recently published January review, WGC analysts noted that the yellow metal did more than finish the month up 8% against the U.S. dollar. “All-time highs were logged across the board in major currencies,” they noted.

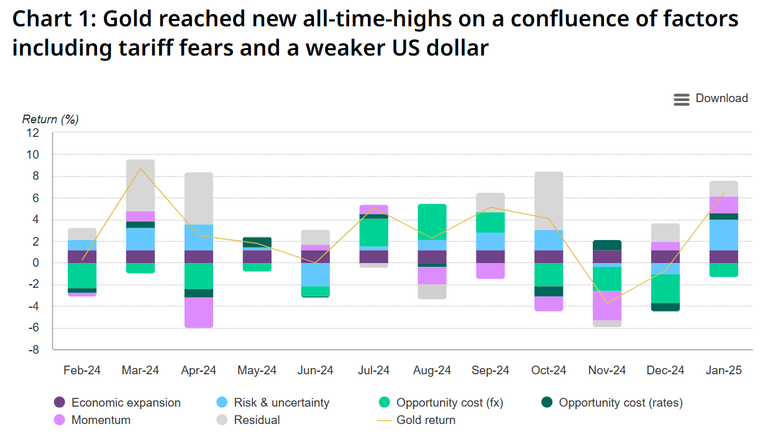

“According to our Gold Return Attribution Model (GRAM), almost all drivers contributed positively including a large rise in the Geopolitical Risk index (GPR), with the only major drag coming from the lagged momentum effect of a strong US dollar in December,” they added.

The ETF picture was also very robust in January, and the demand has now shifted West, though not as far as the United States.

“Global gold ETFs secured a US$2.6bn (30t) gain in AUM, driven almost exclusively by strong inflows into European gold ETFs (+US$3.4bn, 39t) – likely aided by a European Central Bank (ECB) cut that took bund yields down quite dramatically over the course of the month,” the analysts said. “US funds lost US$500mn (6t), Asian funds pared US$320mn (4t) while other ETFs managed small inflows totalling US$51mn (1t).”

The WGC also noted that managed money net longs on the COMEX rose by $64 billion, or 150 tonnes, “with a large increase in longs and a small cut in shorts.”

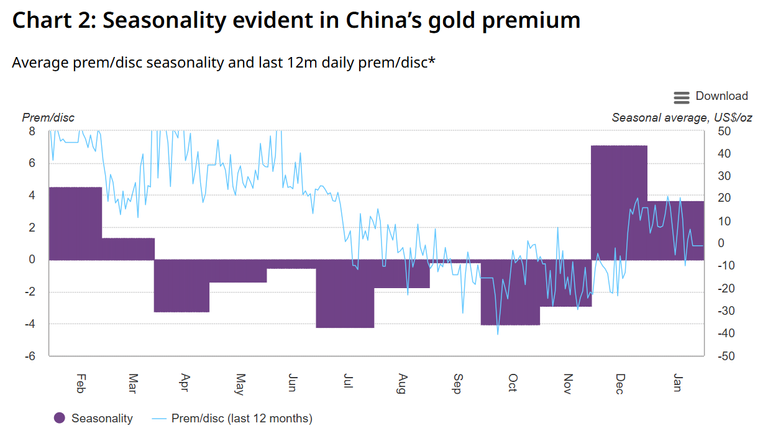

But this is not to suggest that Asia is taking a back seat in the gold market. On the contrary, the Lunar New Year celebrations in China appear to have boosted gold demand despite the record-high prices

“It’s Yisi’s year of the snake in 2025, which occurs every 60 years and promises to be an auspicious one,” the WGC said. “Seasonal strength in local prices was evident in January with an average premium of US$6/oz recorded following several months of discounts (-US$9/oz on average).”

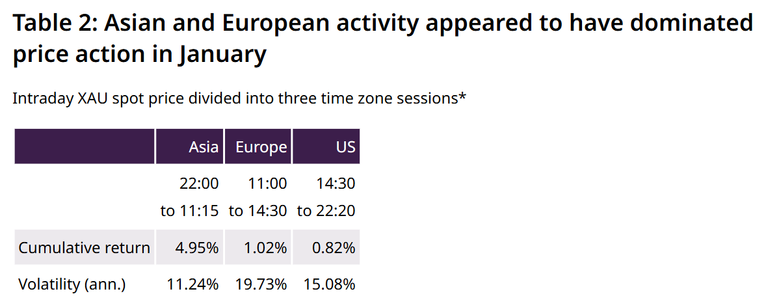

The analysts also said that intraday spot gold price data in January “suggested activity during Asian hours (including the 11am AM price) were instrumental in performance last month.”

“Given that February tends to positively correlate to January, a decent month may lie ahead,” they added. “European gold ETF activity probably also contributed to the session’s strength.”

And while the markets have been consumed by the disruptions caused by President Trump’s first few weeks in office – with tariffs being a particular focus of precious metals traders – the World Gold Council believes that the February 23 elections in Germany could prove very significant.

“Surveys show that the issue German voters care more about than any other, is economic growth,” they noted. “This means that whoever wins will have to deliver. And promises from all candidate parties have been emphatic about delivering on growth.”

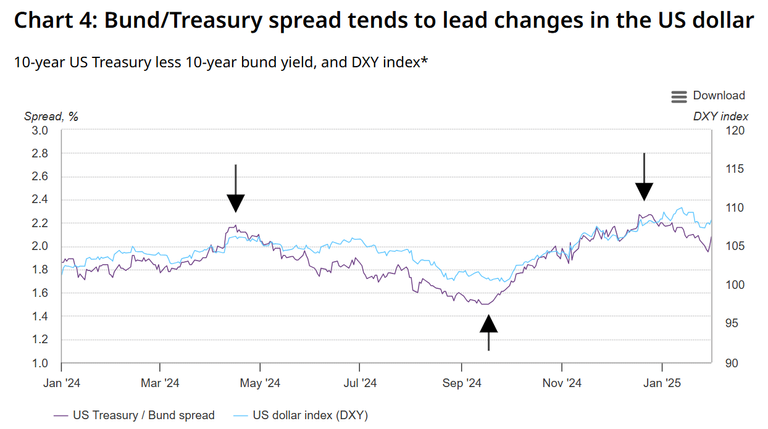

“Equity markets appear to have sniffed out the fruits of a change in administration, with the DAX outperforming most major indices over the past two months,” the analysts wrote. “But next to be impacted may be bund yields. Despite a softer ECB likely lowering short-end rates, stimulus could steepen the curve and pressure longer-term yields higher reducing the gap between bunds and US Treasuries. This spread tends to lead changes in the US dollar index.”

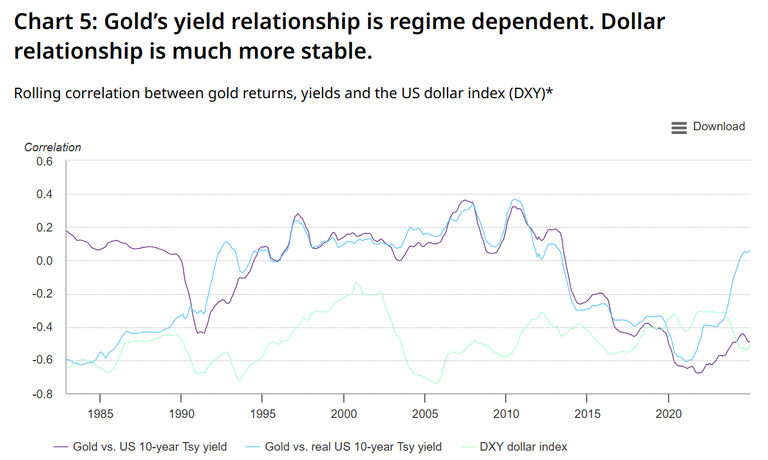

So euro strength could add further pressure to an overvalued US dollar, although it might take a bit of time to materialise and will likely not be dramatic,” they noted. “With the Bank of Japan seeing domestic demand matching targets and further rate hikes tabled this year, we believe a slightly anti-consensus call on the dollar shifting down is a possibility. And gold’s relationship to the US dollar has been consistently negative over the last few decades, more so than bond yields. Although it’s not been key to gold’s price performance of late, we believe a softer trend should provide a gentle tailwind for gold.”

In conclusion, the WGC is looking past the “knee-jerk reaction” from global currencies to Trump’s tariff threats, as “elections in Germany might be a trigger for a sustained strengthening of the euro vs. the US dollar via a contracting Treasury/bund spread” while weakness in the Japanese yen appears less likely.

“All else being equal, US exceptionalism might find a challenge from these two corners, pressuring the US dollar lower – which given the consistent relationship with gold – can add further support to gold’s incumbent strength.”

Posted by:

Jack Dempsey, President

401 Gold Consultants LLC

jdemp2003@gmail.com